Should I get into the market with a deposit lower than 20% or should I wait longer and save a full 20% deposit for my first home?

Our FHBA Coaches are asked the above question by many aspiring first home buyers who are unsure as to whether they should enter the market now with a low deposit or wait until they have saved a 20% deposit. There is no right or wrong answer, it comes down to when you want to get into the market.

In 2024, you can actually avoid paying a 20% deposit and avoid LMI if you are eligible for the FHBG Scheme (for which FHBA is accredited to assist you with)

Disclaimer: Please note our website, including this article, is in no shape or form designed to replace the need to obtain professional advice from experts such as Mortgage Brokers. All information on our website is general & factual in nature and should not be relied upon. In particular, we wish to remind you that the information in this article is not designed to replace advice. We always recommend you speak to a licensed professional. In the examples below, it is important to note that historical price performance is not a reflection of future price performance. Please visit our website’s Terms & Conditions for more information. To speak to a licensed Mortgage Broker please click here.

What is the difference between a 20% deposit and a lower deposit?

Apart from the obvious difference where a 20% deposit is higher than a deposit below 20% (i.e. 5%, 10% or 15%), if you have saved a 20% deposit there is no Lenders Mortgage Insurance (LMI) payable, whereas if you have a deposit of less than 20% the LMI premium applies (some exceptions apply). It is important to note that LMI doesn’t protect the borrower, it protects the lender if the borrower is unable to meet their mortgage repayments. To learn more about LMI, please read our guide to LMI by clicking here. Whilst this is a cost for a first home buyer (it can be added onto your loan in most cases), the lack of Government assistance during the deposit savings phase has meant that a considerable number of first home buyers are forced to enter the market with a deposit of less than 20% of the property purchase price.

It’s a real dilemma for aspiring home buyers, i.e. to buy now, or wait and save. The answer, of course, depends on your personal situation and whether or not you believe where you want to buy is going to increase in value in the future. We take a look at examples below of where first home buyers could be better off and where they could find themselves worse off.

It’s a tough choice! Your FHBA Coach can give you some guidance on which path you should take

The case for ‘paying LMI & buying now’

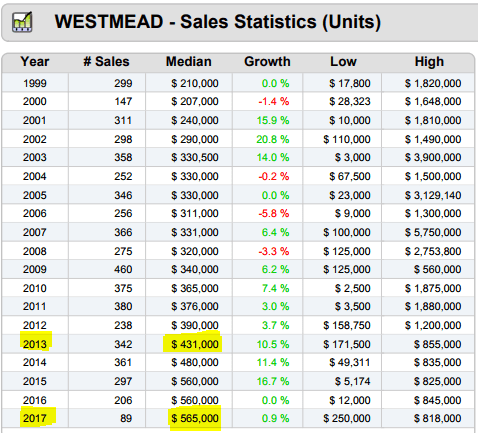

We will use an example of a first home buyer, Tom, who bought his first home in Westmead, NSW in 2013, using a 5% deposit.

Tom paid a 5% deposit in 2013 to get into the market by buying a unit as his first home. Tom anticipated it would take him four years to save a 20% deposit, which is the deposit required to avoid LMI. The table below illustrates the difference in costs of buying in 2013 vs 2017:

| 2013 (5% Deposit) | 2017 (20% Deposit) | |

| Purchase Price | $431,000 | $565,000 |

| Deposit Required | $21,550 | $113,000 |

| LMI (added to loan) | $13,758 | $0 |

| Total cost outlay | $35,308 | $113,000 |

| Initial loan amount | $423,208 | $452,000 |

| Benefit of paying LMI | $120,242 |

As it can be seen from the table above, Tom was significantly better off buying with a 5% deposit in 2013 as prices in Westmead have increased 31% between 2013 and 2017. Tom has benefited by buying in 2013 as opposed to waiting until 2017, the reasons why include the following:

- Tom has experienced a significant $134,000 increase in equity of his first home (as per the below table) – equivalent to 31% increase

- Tom avoided renting as he decided against saving for a higher deposit, he was able to contribute those payments to his own mortgage

- Tom only had to outlay $35,308 in 2013 as opposed to $113,000 in 2017

- Tom’s loan amount is lower now than if he waited until 2017 to buy his first home, as a result of the significant price increase

Historical median price performance of units in Westmead, NSW (Source: APM)

The case for ‘avoiding LMI by waiting & saving for a 20% deposit’

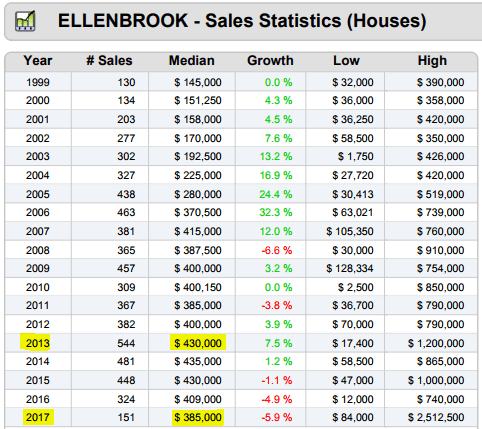

We will use an example of a first home buyer, Samantha, who waited to buy her first home in Ellenbrook, WA in 2017, rather than buying in 2013 with a 5% deposit, an amount she had already saved at the time.

As Samantha decided to wait for her first home purchase, she anticipated that she would have a 20% deposit saved in 4 years time (i.e. 2017). The table below illustrates the difference in costs of buying in 2017 vs 2013:

| 2013 (5% Deposit) | 2017 (20% Deposit) | |

| Purchase Price | $430,000 | $385,000 |

| Deposit Required | $21,500 | $77,000 |

| LMI (added to loan) | $13,726 | $0 |

| Total cost outlay | $35,226 | $77,000 |

| Initial loan amount | $422,226 | $308,000 |

| Benefit of avoiding LMi | $58,726 |

As it can be seen from the table above, Samantha was significantly better off by waiting until she saved a 20% deposit and buying 2017 as prices in Ellenbrook have decreased 12% between 2013 and 2017. Samantha has benefited by buying in 2017 as opposed to buying earlier in 2013, the reasons why include the following:

- Samantha has benefitted by waiting as the median price is now $45,000 lower than in 2013 (as per the below table) – equivalent to 12% drop

- Even though Samantha may have been renting during those 4 years, she had to save $9,000 less as prices dropped $45,000 during that time

- Samantha has saved $58,726 by waiting for 4 years

- Samantha’s loan amount is lower now than if she bought earlier in 2013, as a result of the significant price drop she will ensure her loan is $114,226 lower

Historical median price performance of houses in Ellenbrook, WA (Source: APM)

What should I do, pay LMI or continue saving?

Whilst your FHBA Coach isn’t qualified to provide property related advice, your FHBA Coach can assist you in making an informed decision by advising you of the deposit requirements and the LMI that would apply if you purchased your first home with a deposit of less than 20%. Your FHBA Coach can also send you free property reports (including the data illustration examples above) for your preferred suburbs which will give you an indication of how a particular suburb is performing. Simply complete the form below to get started.

To book your complimentary first home loan consultation with an FHBA Coach/Broker, complete the form below:

Written By,

Taj Singh – FHBA Co-Founder

Disclaimer: The information on our website including this page is general in nature and should be solely relied upon. The advertised rates above were true and correct at the time of the publication. The rates do not take into account other fees and charges which you should also consider. The credit license responsible for the mortgage service offered to clients is Mortgage Australia Group Pty Ltd, Australian Credit License (ACL) number 377294, Australian Business Number (ABN) 99 091 941 749. Mortgage Australia Group Pty Ltd is a member of the Mortgage & Finance Association of Australia (MFAA). FHBA Pty Ltd is an authorised credit representative of Mortgage Australia Group Pty Ltd. You should seek professional advice when obtaining finance and purchasing your first property.