This is a comprehensive blog regarding the First Home Super Saver Scheme. You should consider your own circumstances and consider obtaining qualified advice before commencing any contributions.

First Home Super Saver Scheme gets passed

Announced by Treasurer Scott Morrison at the 2017 Federal Budget in May, the Coalition Government has finally got the legislation pertaining to the creation and running of the controversial First Home Super Saver Scheme through the Australian Parliament on the 5th of December (the Government’s 3rd attempt). The legislation received Royal Assent on the 13th of December 2017, meaning the Scheme is now a binding law.

The Scheme only just passed by one vote, as both Labor and the Greens voted against the Bill on the grounds that it won’t make a big difference to the housing affordability problem and that it would undermine the superannuation system.

On the passing of the legislation, Assistant Minister to the Treasurer, Michael Sukkar, said “the First Home Super Saver provides a much-needed tax cut to young Australians saving for their first home. From 1 July 2018, first home buyers will be able to withdraw voluntary superannuation contributions they’ve made since 1 July 2017, along with a deemed rate of earnings, to help buy their home. This will give first home buyers a significant leg-up towards saving their deposit, helping them overcome a key barrier for getting into the housing market”.

The Turnbull Government is giving first home buyers a much needed tax cut through the First Home Super Saver Scheme. For more information, visit: https://t.co/vRSlzZIWLS pic.twitter.com/ghrfCNa1ZY

— Michael Sukkar (@MichaelSukkarMP) December 8, 2017

We will use the rest of this blog as a general guide to how the Scheme works. Please note, for the rest of this article we will refer to the Scheme as the “First Home Super Saver” (or the “FHSS“) as per the Australian Taxation Office.

How does the First Home Super Saver work?

The FHSS is a brand new Government Scheme designed to help Australians boost their savings tax effectively for the purpose of buying a first home. Essentially, the Scheme (which has strict rules) allows eligible individuals to build a home deposit inside super at concessional (discounted) tax rates. These concessional tax rates, together with potentially stronger investment returns achieved inside super (rather than saving for a deposit in a typical bank account earning low interest) work together to help individuals save a home deposit sooner (in most cases).

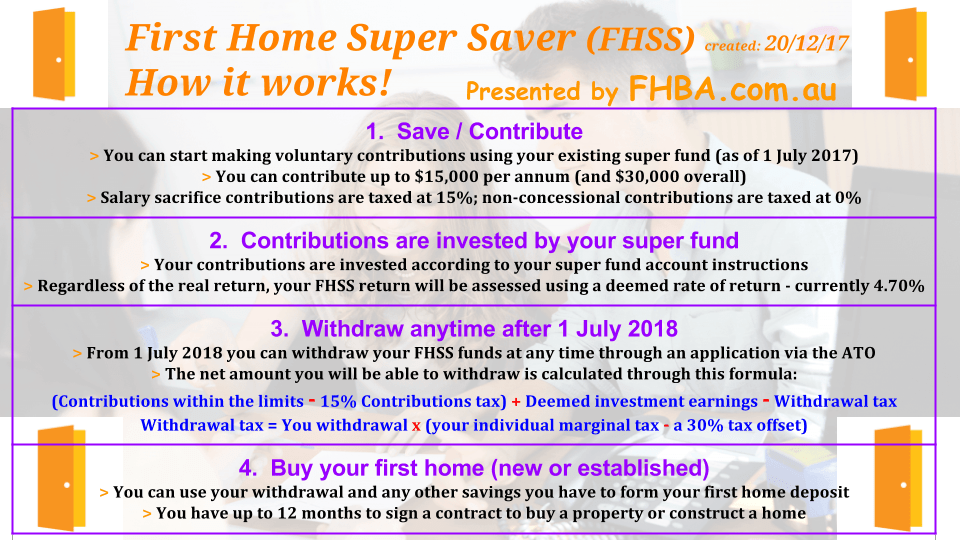

The graphic below outlines the journey of an individual using the FHSS to save a deposit.

What the journey of using the FHSS looks like

First Home Super Saver FAQs

Who can use the First Home Super Saver?

To qualify you must:

- have not previously owned property in Australia*

- have not previously released FHSS funds

- either live or intend to live in the premises you are buying as soon as practicable

- intend to live in the property for at least six months of the first 12 months you own it, after it is practical to move in.

*If the Commission of Taxation determines that you have suffered a ‘financial hardship’ you may still be able to take advantage of the FHSS benefits. The Commission of Taxation will release more info on what a ‘financial hardship’ is before 1 July 2018.

Do I need to setup a new superannuation fund to start?

Most likely no – almost every super fund will be able to accept your FHSS contributions and withdrawal request, but you should double check this with your super fund before you commence making voluntary contributions.

How much can I contribute?

Individuals can voluntarily contribute up to $15,000 per annum (p.a.) and $30,000 in total. Any contributions must be within the existing super contributions caps, currently $25,000 p.a. for concessional (pre-tax) contributions and $100,000 p.a. for non-concessional (after-tax) contributions.

If you are buying with another person, such as a partner or a sibling, each other person can also take advantage of the FHSS as the limits are based on individuals (but note, each individual must meet the qualification criteria).

Contributions above the FHSS limit will remain in your super fund until you reach retirement.

Will you join forces with your partner to save a deposit using the FHSS?

How can I start making contributions?

Only voluntary contributions (i.e. not your mandatory employer superannuation guarantee contributions) can count towards your FHSS.

To make voluntary contributions you can:

- Speak to your employer about salary sacrificing a proportion of your pay: This involves nominating an amount of your pay to be directed to your super fund instead of your bank account. You can choose to start and end salary sacrificing at any time. The amount you choose is up to you, so long as your total financial year salary sacrifice contributions don’t equal more than the $15,000 p.a. limit. Salary sacrifice contributions are considered ‘concessional’ contributions and are taxed at 15% on entry into the super fund (rather than your usual marginal income tax). If you are self-employed you will need to make contributions from

- Transfer your current savings as a lump sum to your super fund: This is a non-concessional contribution and as such these contributions are tax-free. To make a non-concessional contribution simply contact your super fund to see how they can accept these contributions (e.g. they may take electronic transfers, BPay and other methods). Again, remember the $15,000 p.a. limit.

- Self-employed options: If you are self-employed and want to take advantage of the FHSS you will need to make contributions to your super fund yourself. You may be able to claim a tax deduction for these contributions, but we recommend you contact the ATO or your Accountant before claiming this tax deduction.

- A mixture of these options.

How do I make a withdrawal to buy my first home?

From the 1st of July 2018 you can make a FHSS withdrawal at anytime. To make a withdrawal you will need to complete a withdrawal request form with the Australian Taxation Office (ATO). On receipt of a withdrawal request the ATO will:

- Calculate your eligibility (against the criteria outlined above);

- Work out your withdrawal amount (using the formula below);

- Notify your super fund to process your FHSS withdrawal;

- Take out the withdrawal tax (using the formula below);

- Transfer to your nominated bank account your net (after-tax) FHSS withdrawal.

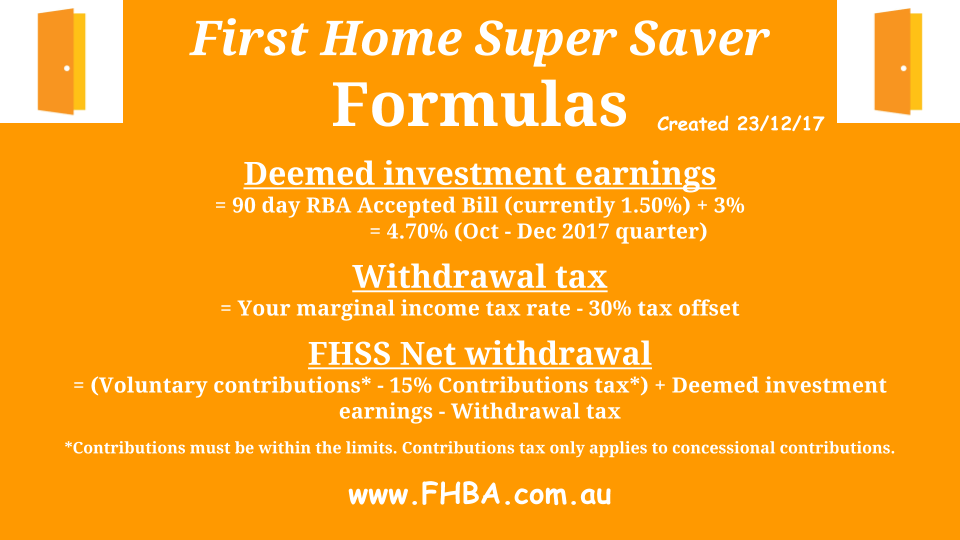

These are the forumlas the ATO will use:

FHSS formulas (above)

You don’t need to remember these forumlas as the ATO will do the processing. The main thing you will need to remember is the contribution limits.

Once you receive your withdrawal you will have 12 months to buy your first home. If you do not buy your first home in this period you will either need to request an extension (up to 12 months), re-contribute the FHSS withdrawal amount or pay tax of 20% on the withdrawal amount (which is designed to remove the tax benefit you received for using the FHSS).

HOT TIP: An FHBA Coach can help you with your FHSS withdrawal when you utilise our FHBA Mortgages service at no charge to you.

Does it matter what type of property I want to buy?

You can use your FHSS withdrawal to buy a ‘new’ or ‘established’ residential property. This includes vacant land if you are planning to build. Properties excluded include commercial properties, houseboats and motor homes.

The home you purchase must not be for investment purposes. You must occupy the property for at least 6 months in the year after purchase (or construction).

Will I really be better off saving my home deposit under this Scheme?

One of the controversial points of the FHSS relates to the complexity of the FHSS. This has resulted in many Australians asking questions like “will I really be better off saving for my deposit using the FHSS?”‘

The Government uses this case study to prove the benefits of the FHSS for an average person.

Elizabeth earns $60,000 a year as a teacher and wants to buy her first home. Using salary sacrifice, she annually directs $10,000 of her pre-tax income into her super fund, increasing her balance by $8,500 p.a. (after the 15% contributions tax has been paid by her super fund).

After 3 years, Elizabeth is able to withdraw $27,380 of contributions and deemed investment earnings on those contributions. Her withdrawal is taxed at her marginal rates (including Medicare levy) less a 30% offset. After paying $1,620 of withdrawal tax she has $25,760 that she can use for her deposit. She has saved around $6,240 more for a deposit than if she had put her savings in a savings account with her bank.

Elizabeth’s partner, Stephen, has the same income through his job in advertising and he also salary sacrifices $10,000 o.a. to his super fund over the same period. Together, Elizabeth & Stephen have $51,520 they can put towards a home deposit, $12,480 more than if they had put their savings in a bank account.

As you can see in this example of two individuals on fairly average incomes, the financial benefit is considerable.

Are your circumstances different to this case study? The Government has created an online FHSS Estimator to help individuals estimate how much better off they will be using the FHSS to save for a deposit – try the FHSS Estimator.

The Government has created a free online tool so that you can estimate much more you will save under the FHSS

The cap is too low, what should I do?

When the FHSS was announced at the May Budget one of the biggest complaints was “the cap is too low, it needs to be bigger”. Unfortunately, other than complain to the Government about this, there is not much we or you can do about this.

But what you can do (if you want) is utilise the FHSS Scheme up to the maximum limit and then save the remaining part of your deposit elsewhere, such as an online savings account or term deposit.

For example, couple Michael and Amy want to save a deposit of $100,000 for their dream first home over three years. They both salary sacrifice $10,000 per annum of their pre-tax wages to their own super fund (total combined FHSS contributions over 3 years equals $60,000). In addition, they save any excess funds they have every month to a joint online savings account. After 3 years they have their $100,000 deposit ready to go, consisting of an FHSS proportion (approximately $60,000) and their joint savings account (approximately $40,000).

Will using the FHSS to save my deposit effect my eligibility for the First Home Owners Grant (FHOG)?

No, not at all. The First Home Owners Grant (FHOG) is based on state law. There is no connection between the FHSS and the FHOG’s of each state.

HOT TIP: Please note, individuals who qualify to use the FHSS don’t automatically qualify for the FHOG. If you want to receive the FHOG you will have to apply for your state FHOG separately (and meet your states FHOG criteria). Again, our FHBA Coaches can assist you determine your FHOG eligibility and apply at no cost to you when you use our FHBA Mortgages service.

If Labor wins the next election will they cancel the Scheme? What will happen to my money?

The Labor Party openly opposes the FHSS and they are currently favourite in betting markets to win the next federal election. If they do form government there is no word whether they will leave the FHSS as is, alter it, or remove it completely.

The old First Home Savers Account was introduced by the Rudd Government only to be axed by the Abbott Government. But when the Abbott Government axed the First Home Savers Account, they made provisions so that those who still had an account and hadn’t purchased a home yet could access their account without penalty.

This is speculative only: if the FHSS is axed by any government in the future, we highly doubt that the government wouldn’t allow individuals to access their voluntary contributions without penalty. Please note, there is a small chance that a penalty or cost of some sort may apply and also a slim chance that your contributions will be locked in your super fund until your retirement – this is referred to as a ‘legislative risk’.

Where can I get more information?

- ATO website

- Speak to an FHBA Coach

- Contact your superannuation fund

Conclusion

In conclusion, most individuals who use the FHSS to save a home deposit will see their deposit grow faster than in a regular savings account. However, the FHSS is a little tricky to understand and comes with some risks. It would be wise to seek your own independent advice before making a decision.

At FHBA, we are not currently licensed to advise whether you should use the FHSS or not, but we can help you to understand how it works and answer general questions about the FHSS. Get in touch with an FHBA Coach if you want to know more.

Written By,

First Home Buers Australia